People-Powered Finance.

We offer a different kind of financial infrastructure — one built on savings, grounded in trust, powered by communities, and scaled through partnerships. Investors and entrepreneurs join us to generate impact while building a sustainable and profitable model.

What makes us different? We prioritize participation, monitor groups and their data in real time, and move fast without losing control.

.avif)

When disconnected from savings culture, financial learning, and community governance, credit often reinforces the very vulnerability it claims to solve.

What looks like opportunity can end in over-indebtedness, extractive lending, or the inability to build a stable future. The real problem is not financial exclusion, but inclusion on terms that create dependency instead of autonomy.

.avif)

.avif)

Only through savings can people achieve true independence and build their own future.

.avif)

Here is how we turn that ancient principle into modern action...

Savinco provides

Save, Lend, Learn

.avif)

Groups meet monthly to pool their savings and issue loans within their capacity, using a multiplier of three or four times their contributions.

The principle is simple: savings come first, followed by credit, with learning integrated into every step of the journey.

Facilitator & Educator

Every group is supported on the ground by a Savinco-trained advisor. They ensure the methodology is followed, rules are clear, and learning is constant. Beyond technical oversight, our advisors are catalysts for dialogue—driving participation and strengthening community governance.

They don't just manage; they facilitate better decision-making and resolve conflicts to keep the group moving forward.

Rooted Learning

Every assembly kicks off with a brief training session led by the advisor. From there, members engage in a consistent, proven cycle: save and lend.

This 'learning-by-doing' approach ensures that members aren't just managing money—they are mastering their resources. By making collective decisions, they strengthen both their group’s resilience and their own autonomy.

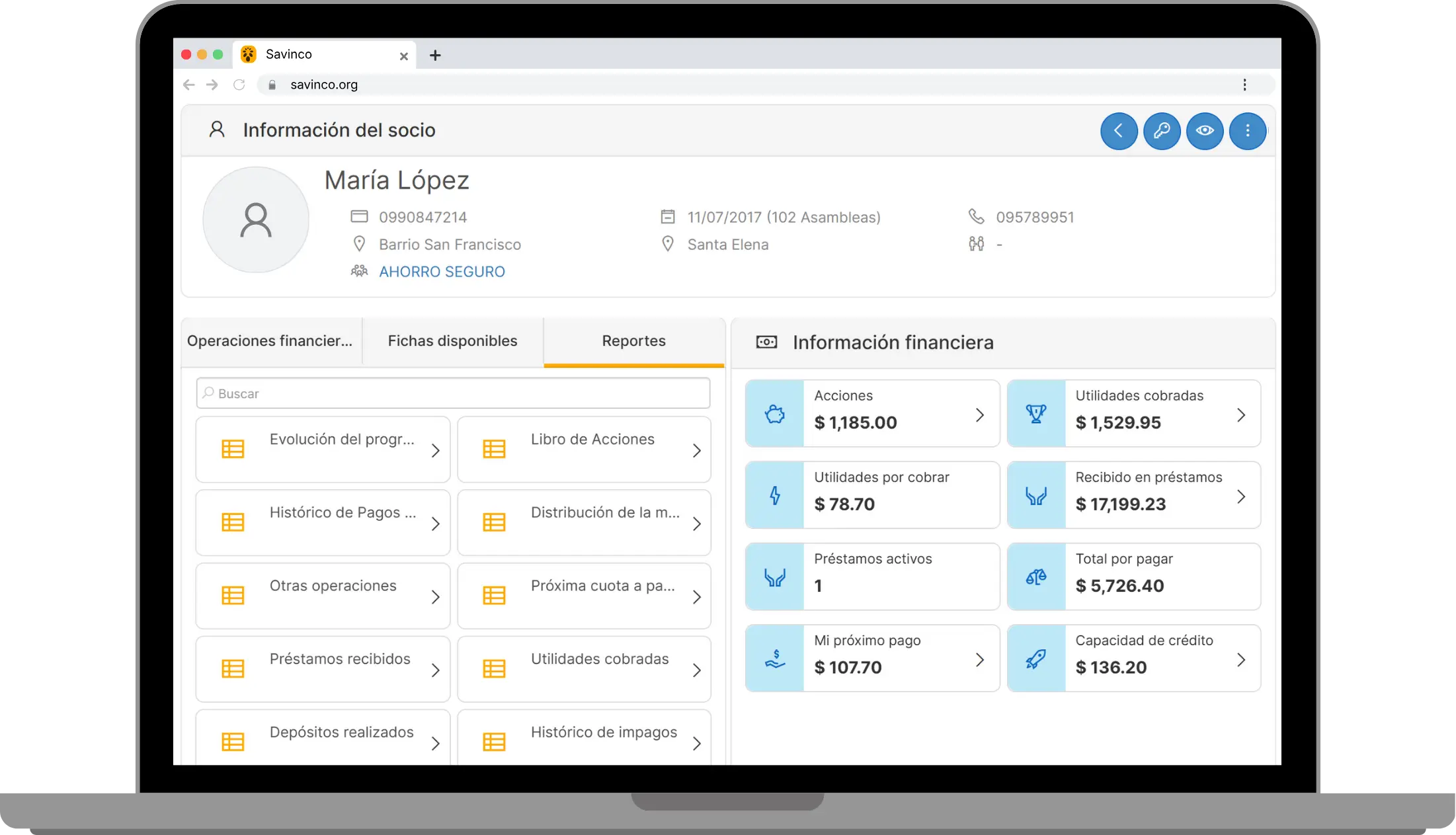

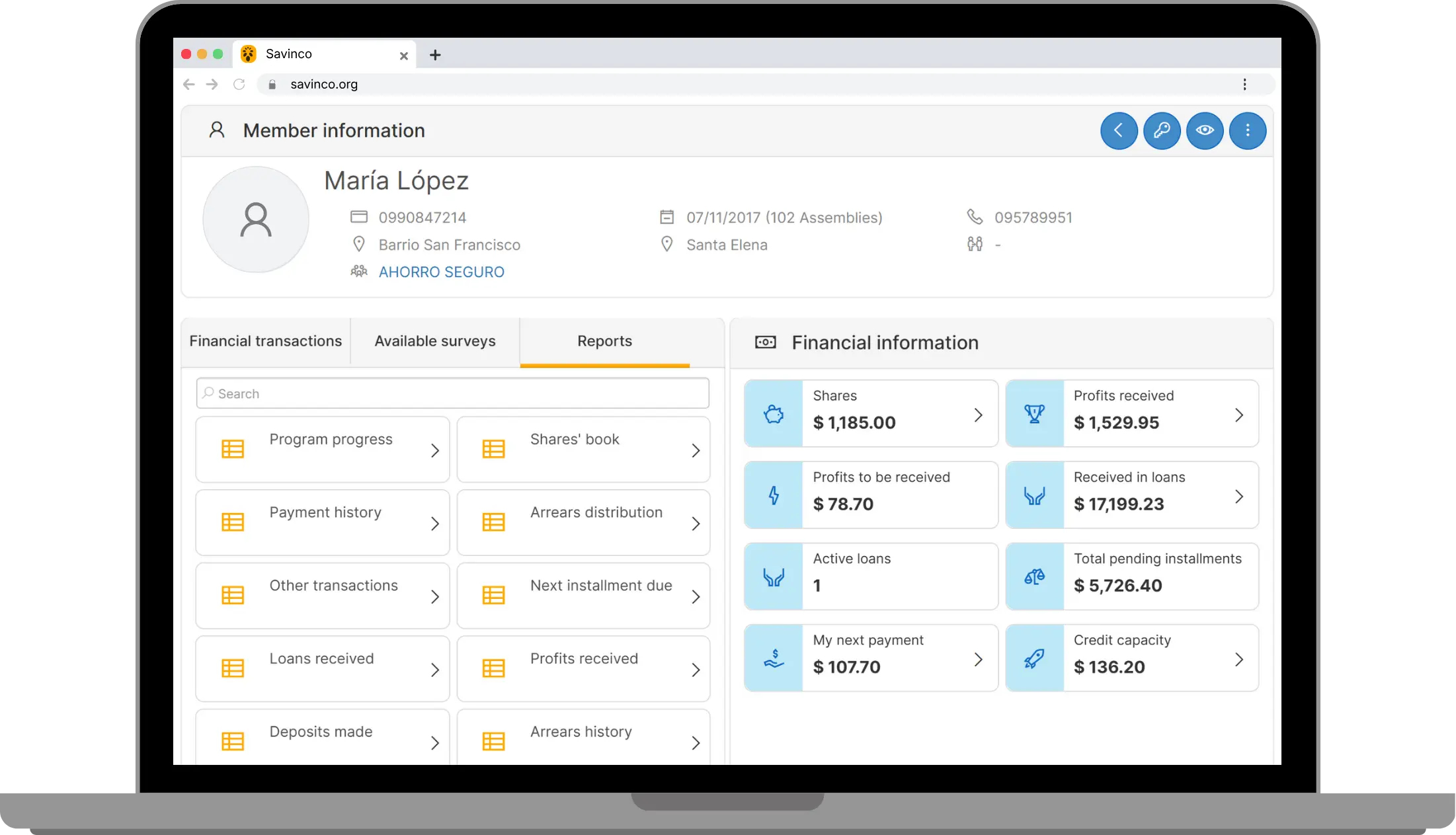

members receive

.avif)

Groups are founded on personal trust rather than collateral, creating financial systems rooted in relationships instead of external guarantees.

Trust is not an accessory but the essential condition that makes savings circulate, loans function, and collective decisions hold. It is the cornerstone of every well-functioning group.

.avif)

By pooling and continuously reinvesting savings, the group generates interest that stays within the community. At the end of each cycle—typically one year—these earnings are distributed back to the members.

We use a sophisticated algorithm for this payout, factoring in both the amount saved and the time it has been invested. These returns are the tangible proof that collective effort yields real rewards.

Powered by

Technology

.avif)

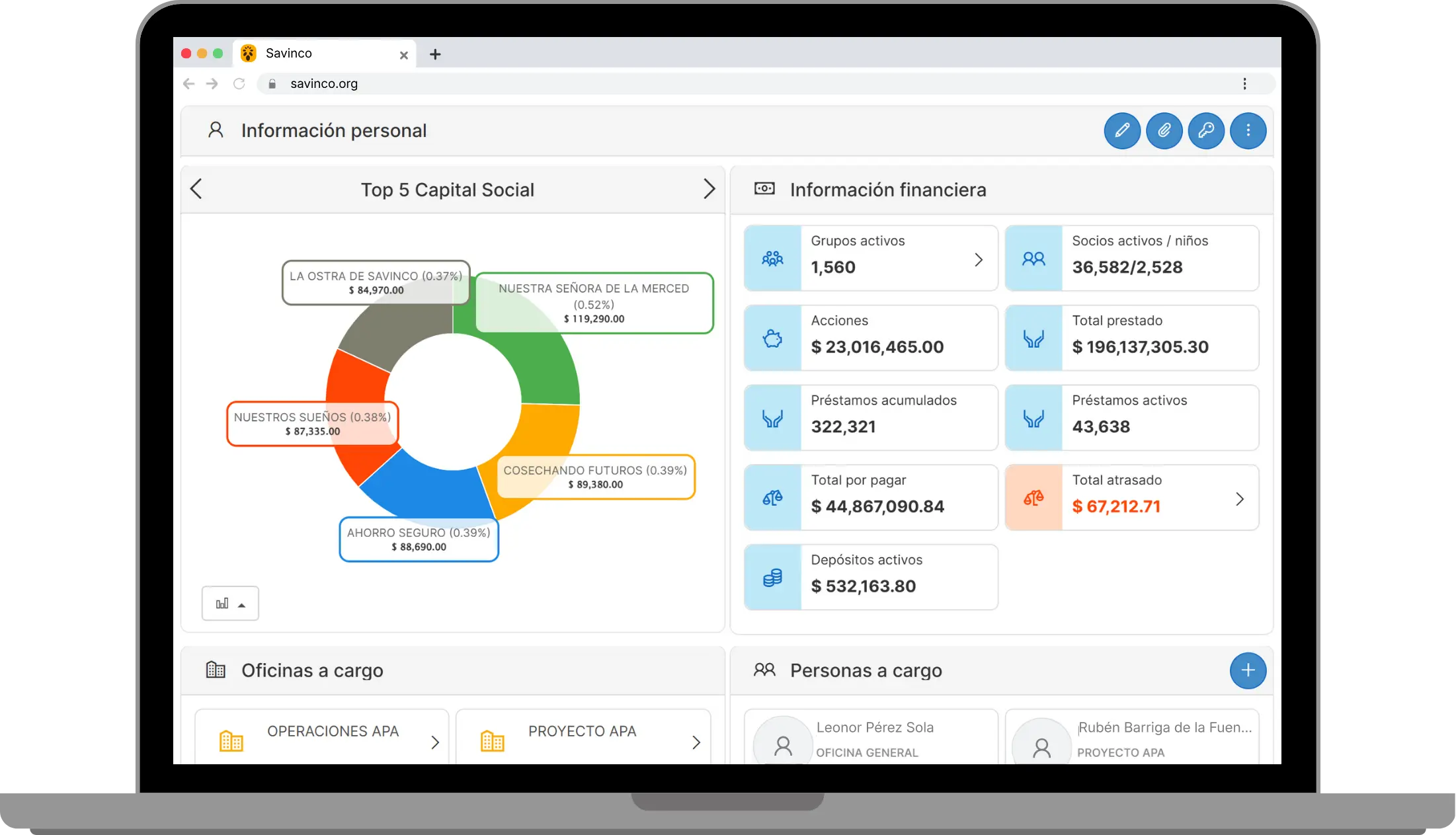

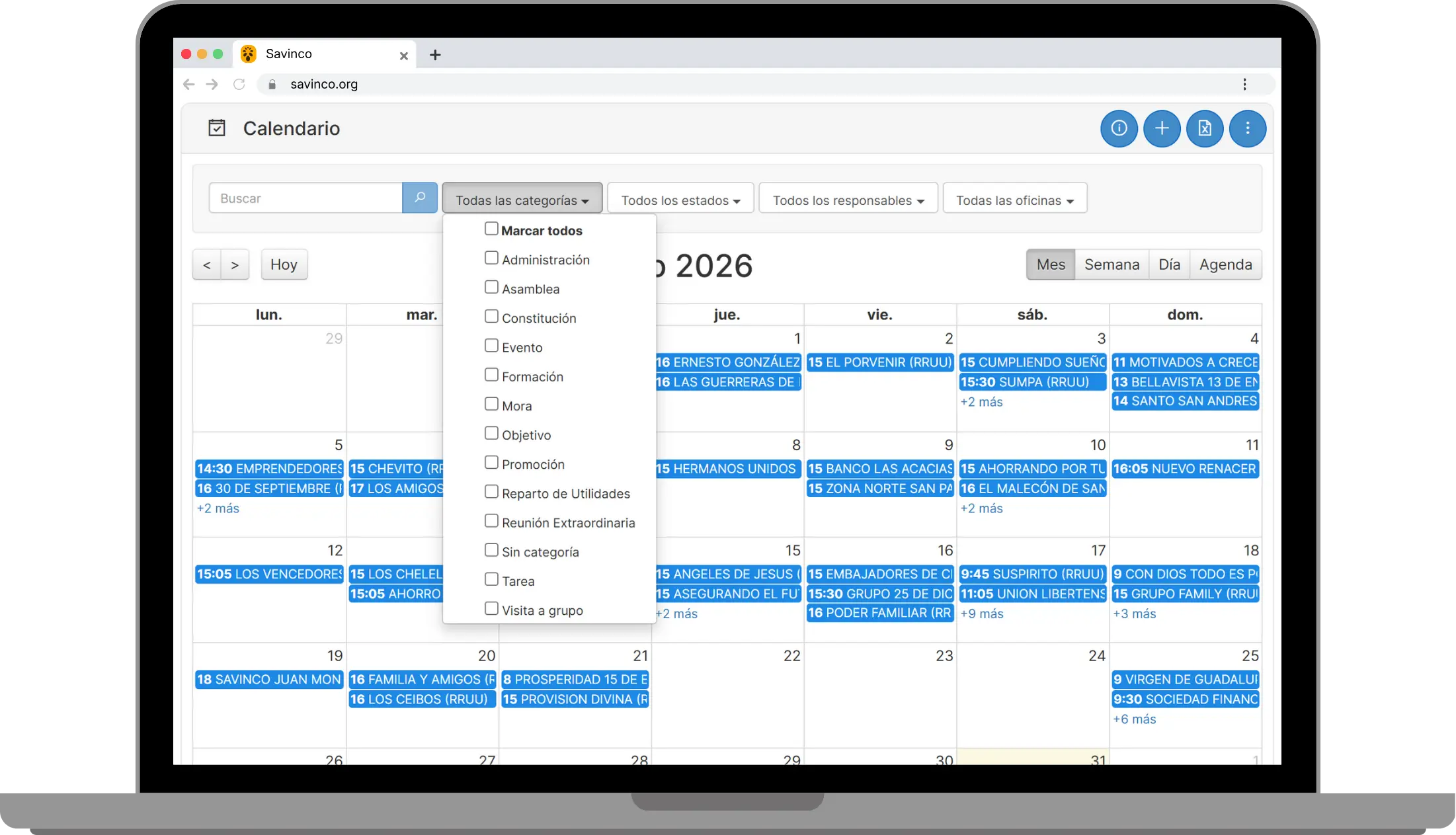

Our advisors log every financial transaction into our proprietary software, ensuring absolute precision and transparency.

We go beyond the balance sheet by capturing qualitative insights: member evaluations, collective decisions, and completed training modules. With a system that updates in real-time, every member has full access to their data right through the App.

Trust is

our currency.

Trust is the foundation of every savings group. It makes cooperation possible, channels resources where they are most needed, and replaces the need for collateral. More than a feeling, trust is social capital: it creates commitment, allows flexibility, and strengthens communities.

Enabling trust in real-time.

All operations — savings, loans, repayments, deposits, profits distributed and others — are recorded in a secure cloud-based system and can be monitored in real time. This not only ensures accountability but also creates a living database of financial behavior.

Through pattern recognition and detailed reporting, our technology allows us to analyze group performance continuously and refine the program, making learning and improvement part of the system itself.

Key features.

Everything at your fingertips...

Get instant insights with regional data, interactive charts, and detailed reporting.

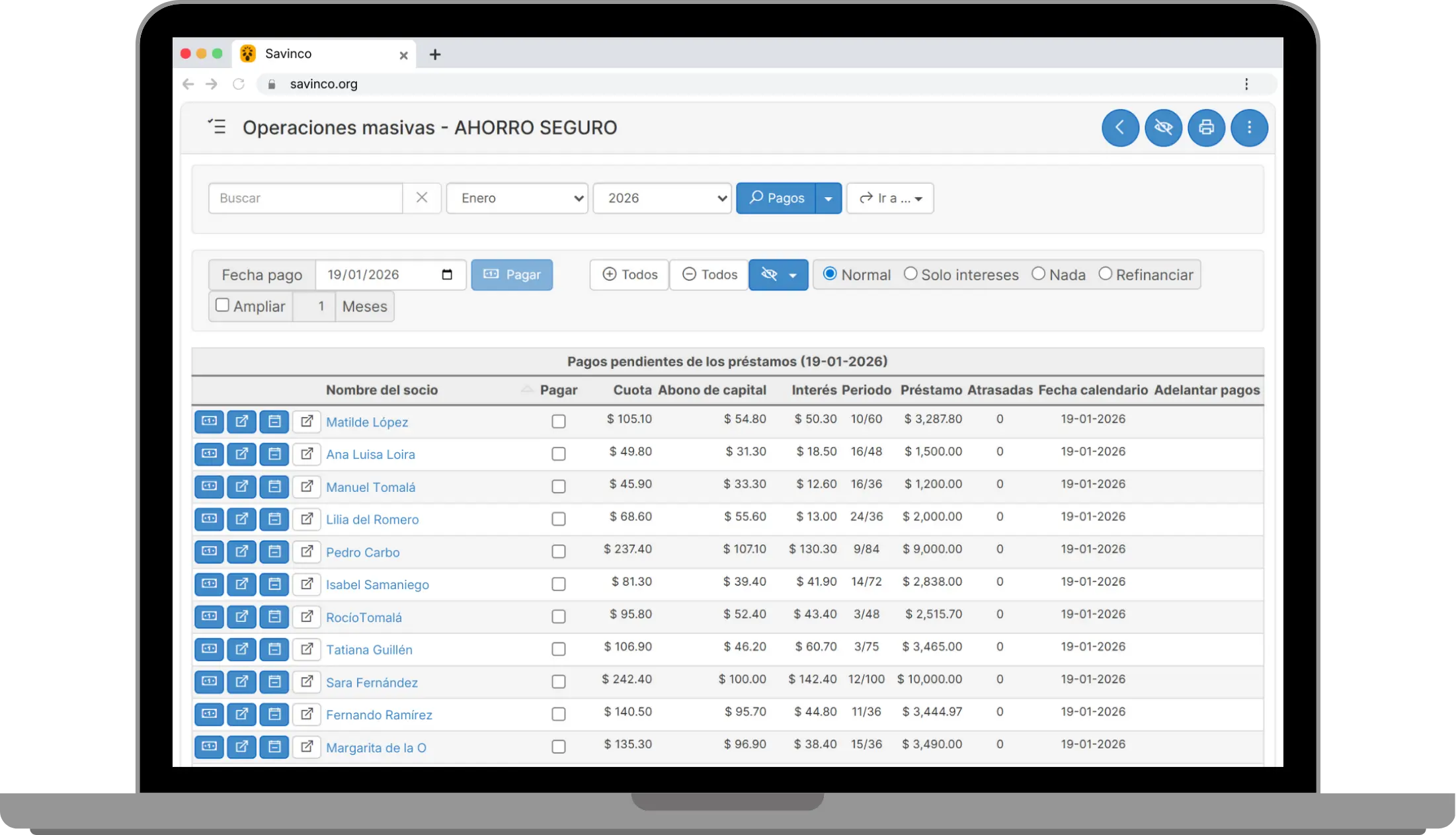

Streamline your team's workflow by recording all monthly group operations through bulk transaction processing.

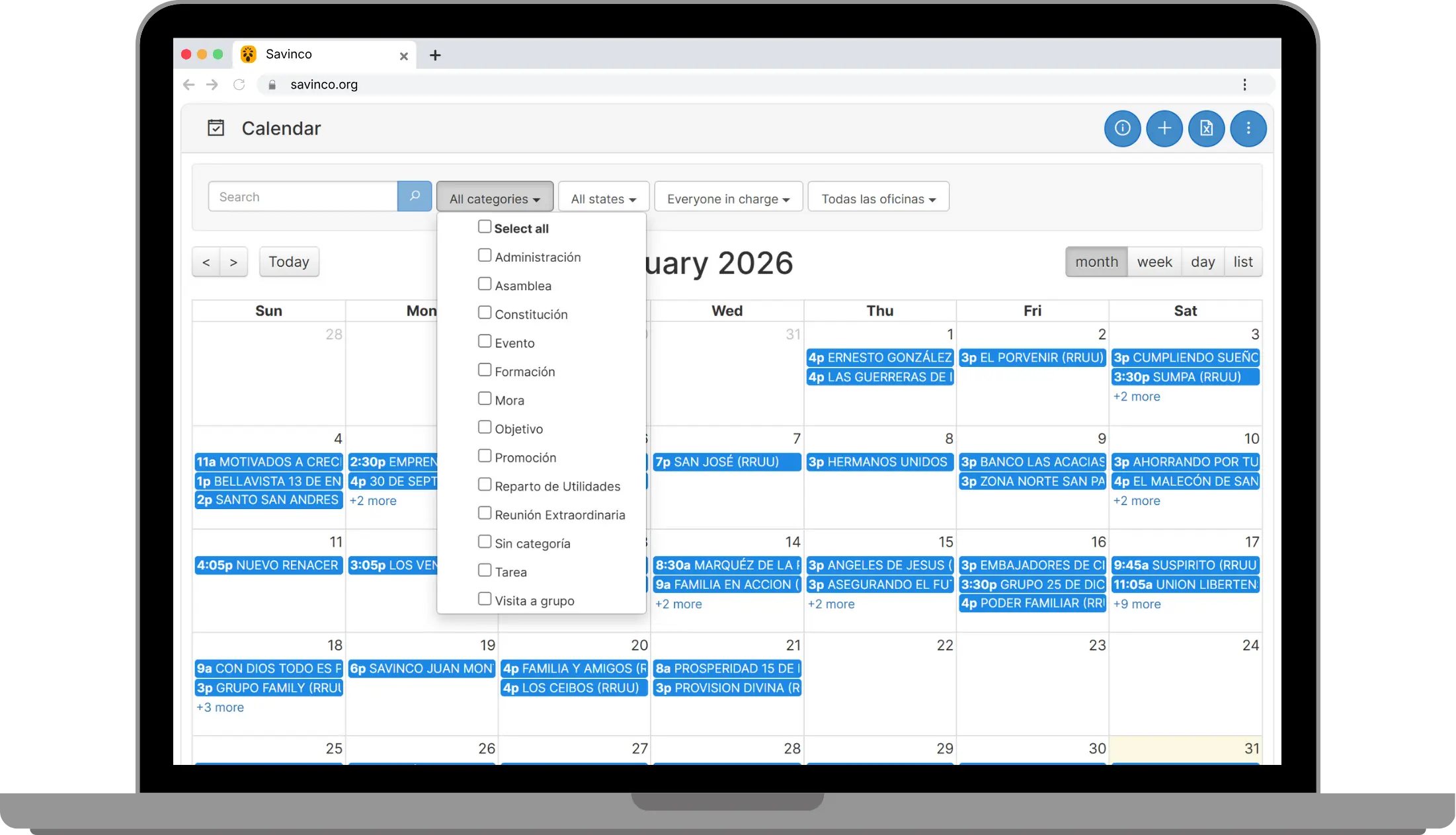

Organize the schedule for assemblies, meetings, and on-site field visits all in one place.

Update client info on the Dashboard and give members instant access through the App.

Frequently asked

questions...

Self-Help Affinity Groups are small, peer-led collectives (usually between 15–40 members) formed by people who share strong social ties. Members voluntarily pool their savings, provide loans to one another, and govern themselves through mutual agreement. These groups emerge organically from trust, shared livelihoods, and community ties, rather than being imposed from outside.

Through regular meetings and democratic governance, members build financial discipline, strengthen commitment, and develop the flexibility needed to support each other in different circumstances. In this way, the model does not just provide access to finance, but creates institutions rooted in trust, resilience, and long-term self-reliance.

Yes. And the reason is simple: trust works as the most powerful contract. Members save first, borrow only within their capacity, and hold each other accountable through clear rules and collective governance.

In Savinco, average arrears are around 0.10%, far below sector standards. In microfinance, maintaining PAR30 < 5% is considered a sign of good portfolio quality, and only a few top institutions report levels close to 0.8–2%. In comparison, our performance is ≈50× better than the 5% benchmark, and ≈8–20× better than the best-documented cases worldwide.

It is not just methodology, or just education, or just technology — it is the combination of all three that makes the model effective.

Groups follow a clear structure, receive financial education, and are supported by Savinco’s team and our own digital tools. Just as important, we constantly observe and adapt: identifying the real problems people face and improving the program accordingly.

All operations — from savings to loans to profit-sharing — are recorded in Savinco’s Qmobile platform. This provides real-time transparency, accountability, and data that allows groups to improve continuously. For Savinco, it also enables scalability: we can support thousands of groups across regions while keeping the model rooted in local governance.

Groups are created when local leaders and Savinco advisors mobilize people who share trust and willingness to save together. Before this, these people receive a complete talk about how the group will work and, if they are committed to start, the first meeting marks the beginning: savings are collected and immediately disbursed in the form of loans.

Groups decide who becomes a member. Admission requires a vote of acceptance, ensuring that new members are trusted and aligned with the group. This principle keeps the group cohesive and reinforces accountability.

Very simply: one member, one vote. All decisions — from loan approvals to rule changes — are taken collectively, ensuring transparency and equal participation. For a vote to be representative and accepted, a majority of members must always be present.

At the end of each yearly cycle, all profits generated from loans are distributed fairly among members, in proportion to both the amount and the timing of their savings contributions. Members who save more, or who contribute earlier and keep their savings working for longer, receive a higher share. This system makes savings productive and ensures that the benefits of lending return directly to those who created the capital.

Advisors guide the group not only in its first cycles, but throughout its entire journey. They ensure that the methodology is applied correctly, provide financial literacy sessions at every meeting, and safeguard transparency and accountability. They also help the group solve problems that may arise and make decisions. Far from being temporary facilitators, advisors remain a constant presence, creating the conditions for groups to keep improving, learning, and growing stronger over time.

Members learn by doing: saving, lending, and making decisions together. Repetition of the cycle makes financial skills second nature and builds confidence over time. That is why the program is called Saving for Learning.

From the very first meeting, groups begin saving and lending, immediately putting into practice the rules they have agreed upon.

Groups do not have a fixed end date. As long as members continue participating in the program and following the methodology, the group remains active. Many groups stay together for years, steadily building more and more capital.

Yes. A member can decide to withdraw, usually by giving at least one month’s notice. This allows the group to plan its cash flow and organize repayments or adjustments with the support of the Savinco Advisor, ensuring the process is orderly and fair for everyone.

True self-help groups are not created to access external benefits. They emerge from trust, shared livelihoods, and mutual recognition. As Myrada’s decades of experience show, groups formed this way endure over time, because their foundation is internal cohesion rather than conditional aid.

From the very first meeting, members save, lend, and learn together. Advisors provide guidance and literacy, but autonomy is built step by step. Regular operations — saving, lending, record-keeping, setting penalties — develop into habits. Over time, groups govern themselves with discipline, high attendance, and repayment norms that consistently outperform microfinance benchmarks.

Trust is more than sentiment; it is the strongest contract. It generates commitment, allows flexibility, and makes collateral unnecessary for most loans. This shared trust not only sustains financial cooperation but also builds confidence, leadership, and collective resilience.

Members save by purchasing shares, which represent the minimum commitment required to be part of the group. Each share has a fixed value decided collectively by the group, and members can purchase one or more at every meeting. This system ensures that saving is regular and predictable, while also flexible enough to match different capacities within the group.

Members can borrow three to four times the amount of their savings (depending on the region). This multiplier system has three effects: it encourages saving, it reduces the group’s risk (since a third or a quarter of the loan is already covered), and it prevents over-indebtedness — the biggest financial trap for low-income families.

Yes, but with limits. A second loan can only be granted if capital is available and no other member is waiting for credit. Even then, the multiplier rule is never broken. This ensures fairness, protects the group, and teaches members to manage credit in line with their real capacities.

Each member decides the repayment period of their loan according to their own needs and possibilities. There are no penalties for early repayment, which allows members to adjust the duration of their loans freely. This flexibility makes the system fully adaptable to household and business realities.

Interest is charged monthly, rather than annually, to match the flexibility required in small community loans. It is calculated using the German method, meaning members only pay interest on the outstanding balance, not on the original loan amount. This makes repayment fair, transparent, and proportional to what is still owed.

We sustain ourselves through a small share of the profits generated by the groups themselves. This creates a direct alignment of incentives: when groups grow stronger and more profitable, Savinco grows with them. Unlike traditional microfinance, we do not earn from interest on loans, but from the prosperity members generate for themselves.

No. There are no membership fees. The only requirement is to save regularly according to the rules the group decides collectively. This way, the capital that sustains the group is entirely generated from within, not imposed from outside.

Savinco combines four elements that rarely work together: a program that begins with savings (not credit), a tested methodology, structured financial education, and proprietary technology. Microfinance often creates dependency through credit. Cooperatives often struggle with governance and transparency at scale.

Savinco brings these pillars together while keeping ownership at the community level. Unlike traditional models, our business model is directly aligned with members’ interests: we do not profit from interest charged on loans, but through a small success fee linked to the groups’ own growth. When groups thrive, Savinco thrives with them.

No. Savinco never handles or intermediates the groups’ money. All capital is owned, managed, and distributed by the members themselves, according to rules they decide collectively. Our role is to provide methodology, education, and technology — not to control funds. This ensures full autonomy and transparency for every group.

A Hub is a physical space that brings Savinco’s model into a specific region in a modular way. Around a Hub, approximately 250 savings groups can be created, supported, and connected. More than an office, it is a platform where methodology, technology, and education converge to scale community finance in one territory.

No. Savinco does not finance or own Hubs. They can be financed fully by partners, or partially with co-investors, depending on the context. What matters is that the financial responsibility and the long-term vision are clearly aligned with the commitment to expand the model.

Savinco provides the framework, methodology, training, and technology that make the Hub function. We also accompany the partner through advisory and continuous support to ensure quality and consistency. However, the implementation and local management belong to the Hub itself.

Yes, in two ways. Once a partner decides to establish a Hub, Savinco charges a one-time implementation fee that covers training, field visits, and full setup over a period of about 12 months. After that, each Hub pays Savinco a small percentage of its revenues. This aligns our business model directly with the Hub’s success: if the Hub grows, we grow with it.

Partners are people who understand the social impact and transformative power of our project and have a genuine interest in bringing it to specific locations around the world. Usually, they have strong ties to that place, and they invest —individually or with others— in establishing a Hub as a high-impact social business.

Implementation is led by a local entrepreneur. It is essential to find someone with the profile, context, and skills to build something from the ground up. Each Hub develops its own internal team, ensuring operations and growth are locally driven.

A possible entrepreneur is someone embedded in the local context, with proven leadership capacity, organizational skills, and the determination to create and sustain a project from scratch. They must enjoy the full trust of the investor partner and be capable of coordinating not just one Hub, but several simultaneously

No. Savinco uses a rigorous evaluation framework to pre-analyze whether minimum conditions are in place for a Hub to succeed. The final decision rests with the partner, but Savinco will not engage in a location where there is no clear sense or potential for impact.

How to build a group, from the ground up.

Community engagement and leadership

Savinco begins by working directly with communities to understand their priorities and dynamics. We identify local leaders who become our key partners throughout the process. Once they fully grasp the project's value, they take the lead in mobilizing the community and organizing the spaces to introduce the project to others, acting as local advocates.

We also collaborate with local institutions that have strong convening power, helping us connect with those most likely to benefit.

Preparing the ground

Supported by the leaders and institutions that gather potential members, Savinco presents the project, outlining its benefits and the commitments involved in joining. Participants then discuss among themselves to decide if they wish to move forward. Having a strong pre-existing bond—whether as family, friends, neighbors, or colleagues—is essential.

Additionally, to ensure the group's dynamism, a minimum of 15 adults is required to start, though children are also welcome to join.

Group constitution

Once the group is formed, members choose a time and place for their first meeting. Savinco assigns an advisor to facilitate the session and provide all necessary materials. During this assembly, a Board of Directors (President, Treasurer, and Secretary) is elected to manage the capital and maintain meeting minutes transparently before the group. Members also establish their rules, including the share value for savings, loan interest rates, and penalties —all formalized with a signature.

Immediately following the meeting, the advisor logs every detail into our platform, ensuring structural order and transparency from day one.

First savings and loans

From the moment the group is established, members save monthly according to their means—for instance, one may save $10 while another saves $30. To ensure balance, no member can hold more than 30% of the group’s total capital. Credit limits are tied to savings: the more a member saves, the larger the potential loan. Applicants must state the loan's purpose and repayment term, with the group collectively deciding on its approval.

Starting from the very first meeting, all capital is immediately mobilized as credit, turning savings into a productive tool for the community. Throughout the process, the advisor guides the group, turning every transaction into a practical financial lesson.